Bitcoin Legislation in North Carolina

I’ve lived in North Carolina my entire life. It’s a great place to live and has a thriving tech scene in the Raleigh-Durham area that has provided me with great employment opportunities. However, despite the local tech scene, the Bitcoin related activity in North Carolina is negligible. Which is why it was quite surprising to learn that a bill has been moving through our legislature that intends to further regulate businesses that handle digital currency. The following is what I’ve learned over the past few months regarding “AN ACT TO ENACT THE NORTH CAROLINA MONEY TRANSMITTERS ACT AS REQUESTED BY THE OFFICE OF THE NORTH CAROLINA COMMISSIONER OF BANKS.”

This bill began its life in the NC House as H289. It was sponsored by three people, but the primary sponsor was Representative Stephen Ross, who just so happens to be an Executive Vice President at Wells Fargo. Surely this is just a coincidence!

After making it out of committee, the bill was then voted on by the House:

Once it was passed by the house it was sent to the Senate with the instructions to rewrite the bill using H289 as a framework. This is where the Banking Commission got involved and created S680. You can read the text of S680 here.

As you can see here, S680 passed its first Rules and Operations committee reading but was sent to the Finance Committee in April 2015 and has had no further action. Luckily for us, S680 did not make it to the floor for a vote during this session, but it will be on the agenda again in Spring of 2016.

S680 was drafted by the NC Banking Commission but then submitted to the Senate by Rick Gunn as the main sponsor. The involvement and process of the Banking Commission in S680 was enumerated in our recent meetup panel that was attended by several Banking Commission representatives. According to the Banking Commission, they have undertaken this proposed legislation at the request of companies that are seeking regulatory clarity around digital currency. The Banking Commission is not willing to name specific companies, but we can connect the dots with some additional public information.

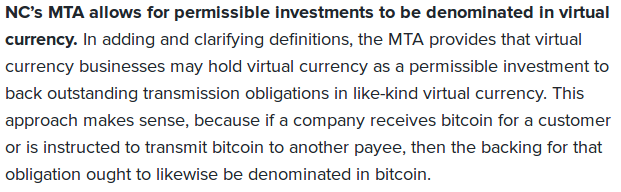

You may recall that Coinbase publicly stated their opinion of NC’s proposed legislation. They noted several of the “positive” points of the legislation, such as:

However, what was not noted was that “permissible investments” only covers the requirements for not operating as a fractional reserve. It does not cover other requirements that I’ll outline later.

Coinbase claimed that “North Carolina is a state promoting innovation and regulatory efficiency into its regulatory framework,” but was this proposal really just due to the foresight and hard work of the NC Banking Commission and NC legislators?

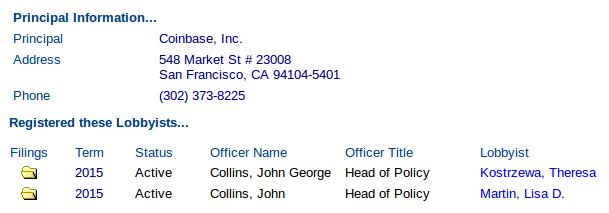

I’ve searched the NC Dept of Secretary of State’s database for every Bitcoin company with more than $10M in venture capital and the only company I can find with lobbyists in NC is Coinbase.

I’ve never hired a lobbyist, but I’m reasonably sure that they are not affordably priced. It appears that Coinbase has not merely been responding to requests from government authorities, but has been actively promoting the idea of enacting additional regulations. From Coinbase’s perspective, investing in lobbyists to enact regulations beneficial to their business is a smart move. But if Coinbase stands to gain, who stands to lose?

Those of us in NC have quite a few concerns about this bill, mainly around how it creates a high barrier to entry for people to innovate in the digital currency space. The Banking Commission says that they drafted this bill due to demand from companies for regulatory clarity, which is a reasonable explanation, except that this bill does not at all clarify which business models fall under the money transmission guidelines and which are exempt. I specifically asked the Bank Supervision Attorney from the North Carolina Office of Commissioner of Banks whether or not BitGo’s non-custodial multi-sig model would fall under the legislation and she couldn’t tell me — it would be up to the Commissioner of Banks to decide. Check out this relevant section from the bill:

§ 53–208.44 (d) The Commissioner may, by rule or by order, exempt from all or part of this Article any person, transaction, or class of persons or transactions if the Commissioner finds such action to be in the public interest and that the regulation of such persons or transactions is not necessary for the purposes of this Article.

The Commissioner has absolute power to follow or ignore any of the regulations set forth in The Articles. What’s the point of all of these regulations if the Commissioner is effectively a dictator who is not constrained by them?

The proposed license requirements are quite onerous just from a financial standpoint, not to mention reporting requirements:

- Net worth: The previous net worth requirement was $100K. This bill increases it to $250K. Additionally, the Commissioner may for any reason increase the net worth required with no cap that I can see.

- Surety bond: A surety bond of $150K is still required and increases based on a company’s money transmission volume with a cap of $250K.

- Permissible Investments and Statutory Trust: Licensees are required to maintain a market value that is no less than the aggregate face amount of outstanding transmission obligations.

- Application fee: This fee has been tripled to $1,500.

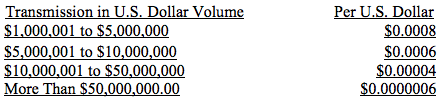

- Annual assessment fee: Raised to a base of $5,000 plus an additional fee for companies with transmission volumes greater than $1M:

It’s worth noting that Xapo and CoinOutlet have already left the state in anticipation of an unfavorable regulatory climate. I suspect that they won’t be the last if this legislation passes.

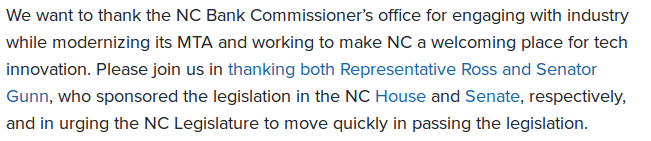

I hope this information is sufficient to gain the community’s interest. You may not care about North Carolina, but whatever happens in these first states proposing Bitcoin regulations will likely serve as a model for future states. We are already working with the Chamber of Digital Commerce to craft amendments that would exempt a number of entities and activities from this legislation, but I’d much prefer a multi-pronged approach; my preference would be to see this go the way of California’s AB-1326. I’m calling upon the EFF, the Bitcoin Foundation, Coin Center, and anyone else in the Bitcoin community with experience fighting legislation to lend their support. We can use all the help we can get.

Update: in December 2015, the North Carolina Office of the Commissioner of Banks updated their FAQ to exempt digital currency miners, non-financial blockchain services, and non-custodial wallet providers from the state’s Money Transmitters Act. Hopefully this means that they don’t find it necessary to amend the existing legislation.